How Payday Loans Shape California’s Economy

The Role of California Payday Loans: Balancing Access and Stability

California payday loans are short term high interest loans aimed to cover borrower’s expenses until their next payday. In California, the economic landscape has resulted in many individuals applying for payday loans for quick cash.

These loans are an urgent financial solution for unexpected medical bills, car repairs, utility bills, or other emergencies. In California, payday loans have become integral to the financial landscape. The diverse economic needs of California residents contribute to the prevalence of payday lending.

This article will comprehensively analyze the economic impact of payday loans on California and individual financial wellness and will include relevant statistical findings.

The Impacts of Payday Loans in California

1. Access to Funds for Underserved Populations

Easy accessibility is the primary benefit of payday loans. Many individuals have limited access to traditional banking services due to their bad credit history. Payday loans come as a convenient option for them to get immediate cash in emergency situations.

Credit checks can be a significant barrier for those with poor credit history, their loans might be rejected due to bad credit score. On the contrary, california payday loans do not require any hard credit check making it easier to get loans without any unnecessary delay. This makes payday loans an essential resource for those who might otherwise be unable to get funds in an emergency.

2. Support for Small Businesses

In many communities, payday loans play a crucial role in the local economy, particularly in regions where banking options are limited and individuals are unable to secure funds easily.

Payday loan businesses employ local residents and often engage in community activities, thereby supporting the local economy.

The presence of payday loan businesses in economically weaker areas can provide a source of employment and economic activity. It can also help small businesses grow by helping them financially when needed. However, business owners should carefully consider the costs associated with payday loans and understand all the terms and conditions before taking one.

3. No Collateral Required

Most loans involve funds being given in exchange for collateral (certainly a vehicle or property). Unlike other loans, payday loans do not require collateral, such as a car title or home equity, to qualify. The requirement of collateral can also be a significant barrier to accessing funds for individuals who may not have assets to give as security for a loan.

The absence of collateral requirements makes payday loans more accessible and convenient for those who do not own valuable assets but need urgent money.

Impact on Individual Financial Wellbeing

1. Improved Financial Management Skills

By understanding the total costs and planning timely repayment, borrowers might become more responsible in managing their finances and avoiding unnecessary debt in the future. The high cost of payday loans might cause borrowers to budget more carefully after properly understanding the terms and conditions before taking a loan.

Those who successfully manage their payday loan repayment become skilled in budgeting and finance management. Understanding the high interest rates associated with these loans can motivate borrowers to explore other financial solutions and adopt more disciplined financial habits.

2. Short Term Financial Relief

For individuals struggling with a financial crisis, payday loans can be a quick cash solution. These loans can cover unexpected expenses such as medical bills, car repairs, and utility bills, preventing severe financial consequences. This short-term, immediate financial relief helps maintain stability in their life.

For example, a borrower might use a payday loan to pay an urgent utility bill, ensuring they can continue working and maintaining their income with a stable mental wellness. This kind of financial support helps individuals avoid the severe consequences of economic crises, where one problem leads to another, potentially more severe.

3. Avoidance of More Costly Alternatives

Individuals may turn to more costly alternatives to meet their financial needs, such as credit card cash advances, collateral exchange, or unregulated online lenders. These alternative options often come with higher interest rates, fees, and risks, increasing borrower’s financial challenges.

On the other hand, california payday loans offer a relatively affordable option for individuals facing immediate cash shortages, providing a bridge to their next paycheck without the extra costs associated with other forms of credit. By choosing payday loans over more expensive alternatives, borrowers can minimize the long-term impact on their financial wellness.

4. Financial Resilience

Payday loans act as a financial safety net for individuals who lack sufficient savings or access to other sources of loans. These loans provide security against unexpected expenses or emergencies, allowing borrowers to address financial crises promptly and avoid long-term severe consequences.

By having access to payday loans, individuals can better prepare for certain circumstances and reduce the impact of financial shocks on their overall wellbeing. This proactive approach to being prepared for an emergency situation can contribute to greater financial resilience and stability.

What Type of Payday Loans do the People in California prefer?

According to California payday loans law, the maximum amount of money one can receive is $300. By the law, for every $100 you borrow, $15 is charged. It means that out of $300, $45 is the amount of your loan fees. So, the maximum sum of money you can receive is $255.

However, this rule is not applicable to installment loans, which are another form of short term borrowing. Unlike payday loans, installment loans do require a better credit history. Installment loans typically involve borrowing a larger sum of money and repaying it over a longer period.

Subtracting the loan fees from the loan amount leaves the borrower with $255. The actual cash received by the borrower is $255 after the loan fees have been deducted. So, California residents usually prefer a $255 payday loan online.

Research Findings:

1. Payday Loan Usage is Popular in California

According to the California Department of Business Oversight, millions of people take payday loans each year in each state. The average payday loan amount is around $300. Most borrowers take out multiple loans throughout the year. This high usage indicates a strong demand for such financial solutions.

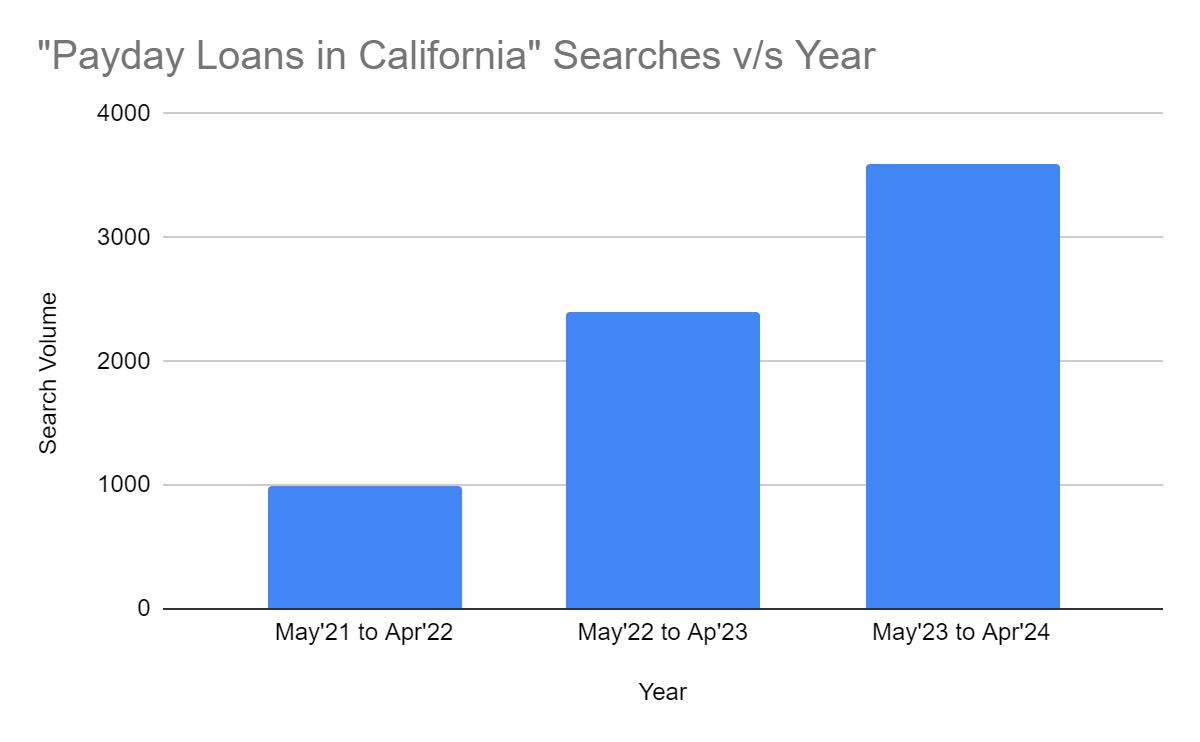

Also, with the expanding market size of payday loans in the U.S., the average monthly searches have also been found to increase.

2. Borrower Demographics

Research observed that payday loan borrowers are often low-income individuals, with many earning less than $30,000 per year.

In 2021, a report given by the Department of Financial Protection & Innovation stated that 49 percent of payday loan customers had average annual incomes of $30,000 or less, and 30 percent had average annual incomes of $20,000 or less.

A significant portion of borrowers consists of minorities as well, highlighting the importance of payday loans in providing financial services to underserved communities.

Conclusion:

While payday loans are often controversial for their high interest, they also provide essential and convenient financial services to underserved communities.

Payday loans are useful in case of urgent cash need when an individual faces any kind of financial emergency. In California, payday loans play an important role in the economy by offering short-term financial relief, supporting small businesses, and contributing to the local economy of the state.

A $255 payday loan online is a popular option for the residents of California because of its overall cost and additional fee. By understanding both the positive and negative impacts of payday loans, consumers can make informed decisions about their use and regulation.